{kind=link}

- 51% of women prefer low-risk financial instruments like fixed deposits and savings accounts, while only 7% invest in stocks

- Half of the salaried women surveyed have never taken a loan

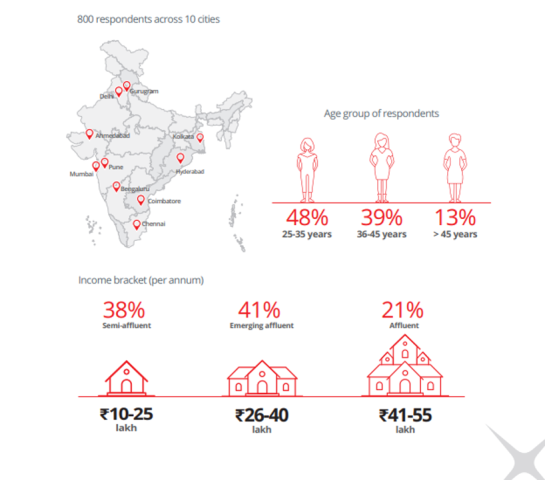

INDIA: In a pioneering effort to understand the way urban Indian women plan, prioritize and manage their money, DBS Bank India, in partnership with CRISIL, has undertaken a comprehensive study entitled ‘Women and Finance’. The first of three reports was launched today, based on the survey that was designed to reveal the financial preferences of women, both salaried and self-employed, across various life stages. Over 800 women were surveyed across 10 cities in India on a wide range of behaviors, including their involvement in financial decision-making, goal setting, saving and investing patterns, and adoption of digital tools as well as their preferences for different banking products.

In the context of the stagnating rate of female participation in the workforce and a persistent gender pay gap, the insights from this study are pertinent for businesses, regulators, and financial institutions as well as a revelation when it comes to understanding the variations of Indian women’s relationship with their finances. The survey findings pointed to factors like age, income, marital status, presence of dependants, and home location as major influencers of the financial behavior of women.

Decision-making dynamics and evolution of goals

Whether it’s charting out their children’s educational paths or balancing multiple, competing financial goals, women are not bystanders, but are at the helm, shaping the future of their families. An encouraging 98% of salaried and self-employed Indian women actively participate in long-term family decision-making. The findings revealed that about 47% of them make independent financial decisions, a reflection of women’s growing financial autonomy. Age and affluence play a pivotal role in shaping these decisions. Women over 45 years old, with their wealth of experience, emerge as the leaders, with 65% making independent financial choices compared to 41% of those aged 25-35 years.

The report provides a fascinating glimpse into the growing empowerment of earning, metropolitan women. Across India, a woman’s primary long-term financial priority evolves with age. Buying/upgrading a home is priority number one for those between 25-35 years, while it evolves to children’s education for those in the 35-45 year category and to medical care for those above 45 years of age. Expectedly, retirement planning is seen entering the consideration set for the first time in the 35-45-year age cohort.

Prashant Joshi, Managing Director and Head of the Consumer Banking Group, at DBS Bank India, said “The insights from the survey highlight the importance of financial stability in the aspirations of independent female earners across India. Ownership of financial decision-making, diverse investment and borrowing choices, and growing adoption of digital channels are all evidence that the modern Indian woman is not just a participant, but a planner of her journey. More than 35% of our own DBS Treasures customer base are female and we have seen many inspiring examples of how women can take charge of their finances. The DBS Women and Finance study is a step forward in the much-needed movement to a more equitable financial playing field and it underlines our commitment to enabling all customers to ‘Live more, Bank less’.”

Saving, borrowing, and investment behavior

Women earners in the metros tend to be risk-averse with 51% of their investments parked in fixed deposits (FD) and savings accounts, followed by 16% in gold, 15% in mutual funds, 10% in real estate, and just 7% in stocks. This tracks behaviors from DBS Bank India’s customer insights where 10% of female customers have an active fixed deposit, while just 5% of male customers have opened an FD.

The presence of dependents understandably plays a major role in women’s investment behavior. Specifically, 43% of married women with dependents conservatively allocate 10-29% of their income to investing, while in contrast, a quarter of married women without dependents choose to invest over half of their income. Regional variations lend greater depth to the insights. For example, Hyderabad and Mumbai lead the way in credit card usage, with 96% of women in Mumbai relying on credit cards, while only 63% of women in Kolkata use them. More significantly, the report revealed that half of the salaried women stated that they had never taken a loan. Among those who have borrowed, the majority opted for a home loan, which reflects the deep cultural importance associated with homeownership in India.

The study also deep-dived into women’s usage of different banking and payment channels. 33% of those in the 25-35 age bracket prefer to use UPI for online shopping, while only 22% above 45 years use UPI. This finding aligns with the customer profile of Digibank by DBS, the mobile-first, digital bank where more than 78% of the female user base is below 40 years of age. The report showed that UPI stands out as the preferred choice for urban women for a variety of payment needs: money transfers (38%), utility bills (34%), and e-commerce purchases (29%), signaling decreasing dependency on cash. Although regional nuances were stark in some cases with only 2% of women in Delhi opting for cash payments, while 43% of women from Kolkata favoured this option.

DBS has been a part of India’s journey since 1994, and it is the largest foreign bank in the country by branch presence with a physical footprint of 530 branches in 350 locations. With the study Women and Finance and its three-part report, DBS Bank India aims to gain a deeper appreciation of the evolving needs and aspirations of women in India to better support holistic financial management and growth.